Insights

Myanmar Government introduces tax deferments and establishes a COVID-19 fund

Apr 07, 2020Summary

Myanmar Government introduces tax deferments and establishes a COVID-19 Fund

The Republic of the Union of Myanmar Ministry of Planning, Finance and Industry issued a notification )(Notification 1/2020 - English and Myanmar version) (the “Notification”) of remedial measures on 18 March 2020. This benefits hotel and tourism companies, small and medium enterprises (“SMEs”) and cut-make-pack (“CMP”) businesses as priority sectors (“Priority Sectors”) for remedial measures.

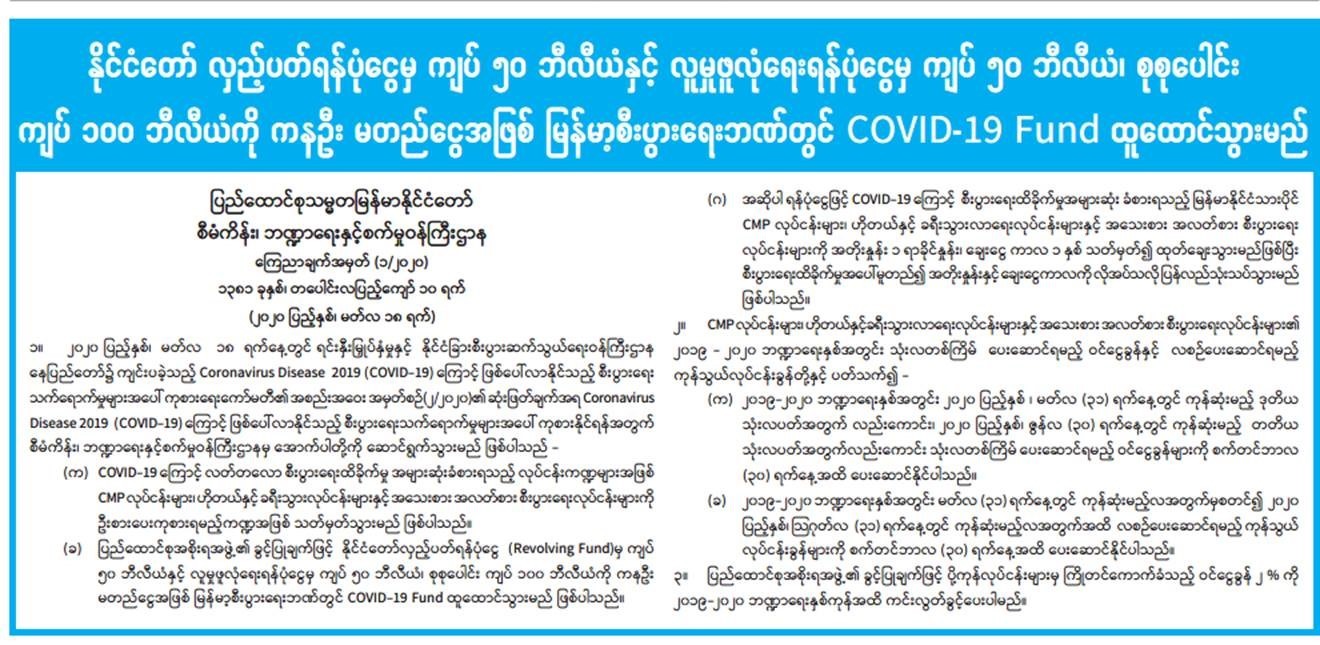

The Notification introduced tax deferrals for businesses in the Priority Sectors and also established a COVID-19 fund to provide loans to the Priority Sector businesses owned by Myanmar nationals.

COVID-19 fund

A COVID-19 fund (the “Fund”) is established and operated by the Myanma Economic Bank with a capital of MMK100 billion (approximately USD71 million), made up of MMK50 billion from the National Revolving Fund approved by the Union Government and MMK50 billion from the Social Security Fund.

The Fund will provide loans to hotel and tourism companies, SMEs and CMP businesses (in each case) owned by Myanmar nationals. The interest rate of such loans will be one percent and their tenures will be one year (the interest rate and loan period may be varied depending on the severity of the economic loss incurred by the applicant). It is understood that the amount of the loan will be considered on a case-by-case basis.

The deadline for applications for such loans is 9 April 2020. Applications can be sent to the Union of Myanmar Federation of Chambers of Commerce and Industry (UMFCCI) and state/regional merchant and industry associations between 29 March 2020 and 9 April 2020. Applications can also be made online starting from 2 April 2020.

Deferred income tax and commercial tax

The Notification specifies that quarterly income tax and monthly commercial tax payable by companies in the Priority Sectors are deferred as follows:

(a) income tax payments for the second quarter due on 31 March 2020 and for the third quarter due on 30 June 2020 (in respect of the 2019-2020 fiscal year) will have their deadlines extended to 30 September 2020; and

(b) monthly commercial tax payments for the period from 31 March 2020 to 31 August 2020 will have their deadlines for payment extended to 30 September 2020.

Under Directive 3/2020 issued by the Inland Revenue, in relation to the above tax deferments, the following entities qualify as SMEs:

(a) if the main business activity is manufacturing, a business which has capital (exclusive of the value of any relevant land) of not more than MMK1 billion (approximately USD710,000) (capital includes capital and own funds contributed as well as loans);

(b) if the main business activity is wholesale, a business whose revenue is not more than MMK300 million (approximately USD213,000) in the previous year;

(c) if the main business activity is retail, a business whose revenue is not more than MMK100 million (approximately USD71,000) in the previous year;

(d) if the main business activity is the provision of services, a business whose revenue is not more than MMK200 million (approximately USD142,000) in the previous year; and

(e) if it is a business other than those listed in (a) to (d) above, a business whose revenue is not more than MMK100 million (approximately USD71,000) in the previous year.

Exemption of advance income tax for export

With approval from the Union Government, two percent income tax levied in advance for export will be exempted until the end of the 2019-2020 fiscal year.

Related Practice Areas

-

Corporate

-

Public Policy & Government Affairs

-

Real Estate

-

Tax & Private Client

-

Hotels and Hospitality

{kind=link}