Insights

UK Corporate Briefing May 2026

May 05, 2026Summary

Welcome to the Corporate Briefing, where we review the latest developments in UK corporate law that you need to know about. In this month’s issue we discuss:

FCA Consultation Paper: Changes to Information Flows for UK Equity IPOs

The Financial Conduct Authority (FCA) has published Consultation Paper CP26/14, which proposes to remove the mandatory seven-day waiting period before syndicate banks can publish connected research on an IPO issuer, and to remove the requirement for syndicate banks to share equal information with unconnected analysts.

FCA review: key takeaways for market sounding practices

The FCA’s review of market sounding practices has found no material impact on market quality but cautioned that the risk of information leakage increases with the scale of the sounding exercise.

FCA Primary Market Bulletin No.62

This edition covers the FCA's enforcement action against Carillion's former directors, concerns regarding manipulative schemes targeting UK small-cap issuers, and observations from the FCA's review of sponsors' work on the modified transfer process.

FTSE UK Index Series – What the New Free Float Rules Mean for Market Participants

FTSE Russell has announced plans to align the minimum free float requirement for non-UK incorporated companies with that of UK incorporated entities. The proposed changes could have significant implications for non-UK incorporated companies seeking index inclusion.

Equality (Race and Disability) Bill

Following strong consultation support, the government has announced plans to introduce mandatory ethnicity and disability pay gap reporting for large employers with 250 or more employees.

FCA Consultation Paper: Changes to Information Flows for UK Equity IPOs

Key Proposed Changes

Removal of the 7-Day Connected Research Delay

The FCA proposes to remove the ‘7-day delay’, introduced in 2018, between the publication of an approved registration document or prospectus and the publication of connected research. Feedback has indicated that these reforms have not delivered on their objective to increase the production of independent, unconnected research on IPOs.

If the proposals are implemented, firms will be able to publish the approved registration document or prospectus and any connected research simultaneously. Under the current rules, connected research must be delayed by one day where the issuer has held a joint briefing with both connected and unconnected analysts, or by seven days in all other cases (which, in practice, has been the default). Removing this mandatory delay will reduce the window during which an IPO is exposed to market volatility and enable UK IPO timelines to compete with those in other jurisdictions.

Removal of Equal Information Sharing Requirements

The FCA also proposes to remove the rules which prohibit connected analysts from communicating with IPO issuers unless syndicate banks first identify a range of unconnected (independent) analysts and ensure that those unconnected analysts are given the opportunity to receive the same information as connected analysts.

In practice, the requirement to share equal information with unconnected analysts is generally met by providing them with the analyst presentation on request, together with any questions that connected analysts have asked of issuers and the responses.

The FCA considers that these requirements have added considerable friction to the overall IPO process and may impede the flow of information to analysts. In particular, the screening of unconnected analysts and ongoing monitoring of the distribution of information by syndicate banks is both costly and complex for issuers, involving significant legal and compliance resource. The FCA is not aware of any similar mandatory information sharing rules in other markets, including the EU.

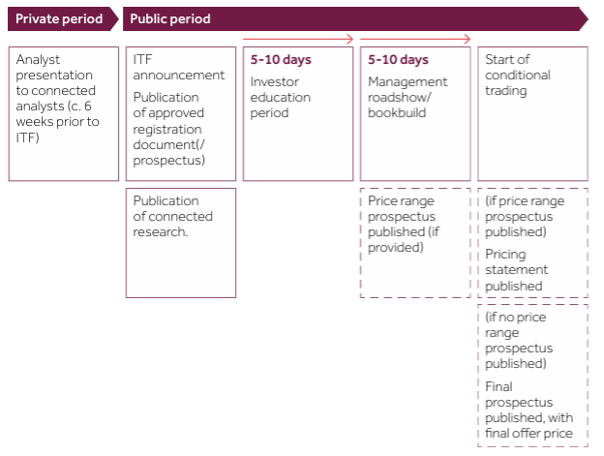

Indicative Post-Implementation IPO Timeline

(Extracted from the FCA Consultation Paper)

Pre-Mandate Analyst/Issuer Communications

The 2018 reforms also sought to improve conduct standards and reduce perceived conflicts of interest in the production of connected IPO research. FCA Handbook guidance was added with the aim of limiting the involvement of research analysts in "pitches" for corporate finance business and protecting the objectivity of analyst research. Although the FCA is not proposing changes to these rules at this stage, it has included discussion questions in the consultation paper to explore whether there is scope for further reform.

Some issuers and firms have suggested that the FCA guidance can be interpreted very conservatively and is overly restrictive compared to other jurisdictions. In particular, issuers have indicated that it is useful to meet with analysts to assess whether they have the relevant expertise to cover their company effectively. For banks, analysts can serve an important role in conducting due diligence on potential IPO candidates based on their extensive sector expertise.

FCA review: key takeaways for market sounding practices

The FCA has published a review examining market soundings across 50 accelerated bookbuilds (ABBs), drawn from 63 transactions conducted by five banks between January 2023 and June 2025. The review found that trading volumes fell by an average of 13% during sounding periods. However, there was no material impact on other market quality metrics and only isolated cases showed any significant increase in trading volumes prior to inside information announcements.

Background

Market soundings are used to gauge investor interest in a potential transaction before it is announced, supporting price discovery and deal sizing. Under the UK Market Abuse Regulation (UK MAR), inside information may be disclosed during a market sounding provided certain conditions are met. The scope of this review was limited to market quality and sounding practices and did not assess compliance with UK MAR or their systems and controls for handling inside information.

The FCA undertook this review after supervisory work identified transactions in which a relatively large number of investors had been approached during the sounding process, prompting the regulator to assess whether such practices were affecting market quality.

Key findings

On average, 33 investors were sounded per transaction, with the largest exercise involving 87 investors. The average acceptance rate among market sounding recipients (MSRs) was 87%, indicating that banks are generally directing soundings at investors likely to participate.

Notably, ABBs that achieved high coverage by approaching an above-average number of MSRs did not result in a meaningful increase in overall demand or oversubscription following launch, suggesting that a smaller sounding exercise may have been sufficient in certain cases.

Governance and controls

All five banks had conducted at least one internal audit covering market soundings during the review period, with some also carrying out quarterly or annual compliance reviews. Issues identified were generally limited to record-keeping errors and no instances of inadvertent disclosure of inside information were reported.

How MSRs handle market soundings: gatekeeper arrangements

The FCA spoke to a number of MSRs about how they handle market soundings in practice. Each MSR had 'gatekeeper' arrangements in place, with the gatekeeper function sitting within either compliance or capital markets responsible for assessing whether to accept a market sounding. Gatekeepers considered factors such as the proposed cleansing process and expected duration of the sounding before accepting. Even where a sounding was declined, MSRs would still place the relevant security or securities on a watch list.

Upon acceptance, MSRs made their own assessment of the inside information received and imposed trading restrictions on the relevant securities. Gatekeepers also identified which individuals/teams within the MSR should receive details of the potential transaction, with initial contact typically made on a no-names basis. Where additional individuals were subsequently brought into the sounding, MSRs ensured that insider lists remained accurate and up to date and maintained clear processes for lifting trading restrictions at the end of the process.

Regulatory implications and next steps

The FCA does not prescribe the number of investors that may be sounded but cautions that the risk of inside information leaking may increase as the scale of a market sounding grows. Firms may wish to evaluate whether their policies and procedures adequately address the scale of their market soundings.

The FCA has indicated that it will continue its supervisory engagement with banks and other market participants, and will take into account the findings of this review in any future changes to UK MAR. Most banks considered the existing regime to be clear, but suggested improvements including greater alignment with the EU market sounding regime and a reduction in record-keeping burdens.

FCA Primary Market Bulletin No.62

Carillion plc — Misleading Statements Case

Key Failings

Carillion, a listed company, recklessly published announcements on 7 December 2016, 1 March 2017 and 3 May 2017 that were misleading. The announcements made misleadingly positive statements about its financial performance generally and in relation to its UK construction business in particular, Carillion Construction Services (CCS), which did not reflect significant deteriorations in the expected financial performance of CCS and the increasing financial risks associated with it.

Carillion's procedures, systems and controls were not sufficient to ensure that contract accounting judgements made within CCS were appropriately made, recorded and reported internally to the Board and the Audit Committee.

The FCA found that Carillion's three former directors — its Group Chief Executive Officer (Richard Howson) and its two former Group Finance Directors (Zafar Khan and Richard Adam) — had acted recklessly and been knowingly concerned in Carillion's contraventions. Despite being aware of the risk that the announcements were false or misleading, they failed to bring these matters to the Board and the Audit Committee. Instead, the information provided to the Board painted a far more optimistic picture than that being reported internally by CCS.

Regulatory Significance

The FCA emphasises that this outcome underlines the high standard of disclosures expected of listed companies, the need to maintain adequate procedures, systems and controls, and the FCA's willingness to hold executives personally to account for issuer breaches — reinforced by the Financial Reporting Council's 2024 UK Corporate Governance Code's introduction of board accountability for effective internal controls at listed companies (new Provision 29 which applies for financial years beginning on or after 1 January 2026).

Manipulative Investment Approaches — FCA Concerns

The FCA has expressed concerns that UK micro-cap and small-cap issuers are being targeted directly as part of potentially manipulative schemes to affect their share prices. Two specific schemes are highlighted:

Fake Investor Takeover Approaches

These are schemes where parties pose as genuine investors seeking to make an offer for an issuer's entire share capital, when those parties are not who they claim to be. These parties may leak news of the supposed takeover online or push the issuer to disclose the approach to the market, with the aim of increasing the share price so they can profit from that movement.

Equity Fundraising Linked to Pump-and-Dump Schemes

These involve an approach to the issuer about equity fundraisings featuring the issuance of large numbers of warrant instruments. The FCA has identified several fundraises carried out shortly before significant upward share price movements and is concerned those movements may have been caused by pump-and-dump schemes involving online advertising containing false or misleading information. Warrants are then exercised and shares sold at the inflated price.

The FCA stresses that it is vital for directors of listed companies and their advisers to carry out appropriate due diligence before engaging with any proposal. This includes:

- clearly understanding who the investors are by verifying their identities through independent sources;

- confirming the investment offer is genuine; and

- reviewing the investors' track record for similar deals.

Review of Sponsors' Work on the Modified Transfer Process

In late 2025, the FCA commenced several reviews of sponsors that had worked on modified transfers into the equity shares (commercial companies) (ESCC) category, focusing on the nature and extent of sponsors' due diligence in supporting the modified transfer declaration, spanning a number of sponsors and a broad variety of transactions and scenarios.

All sponsors reviewed thought carefully about the work required, based on their relationship with the issuer and its recent history. The scope of work varied materially in practice, reflecting different issuer risk, business complexity, and knowledge gained through existing advisory and broking relationships.

In relation to Financial Position and Prospects Procedures (FPPP) reports, the FCA observed sponsors both obtaining and not obtaining a new FPPP report, and considered both approaches appropriate in their specific context. Where sponsors had deep, longstanding relationships with issuers, they relied on this knowledge to justify a more bridging or gap analysis approach.

The FCA was pleased to see sponsors following best practice (set out in Technical Note TN 718.3) in satisfying themselves that directors understood the additional responsibilities and obligations applicable on transfer to ESCC. All sponsors assessed directors' level of understanding and provided tailored training accordingly.

Although sponsors carried out different work, each came to a reasonable opinion after due and careful enquiry, and the work undertaken to provide the positive declarations required by the UK Listing Rules appeared appropriate in each case.

The FCA also observed sponsors diligently following their own procedures, with thoughtful compliance oversight, well-staffed transactions involving knowledgeable individuals, and adequate record keeping across all sponsors reviewed.

The FCA was encouraged to see the modified transfer process being used and sponsors applying their expertise and judgement.

FTSE UK Index Series – What the New Free Float Rules Mean for Market Participants

Key Change: Free Float Requirement

Currently, to be eligible for inclusion in the FTSE UK Index Series, a security must have a minimum free float of 10% if the issuing company is UK incorporated and a minimum free float of 25% if it is non-UK incorporated.

With effect from the June 2026 index review, both UK and non-UK incorporated companies with a minimum free float of 10% will be eligible for inclusion in the FTSE UK Index Series, subject to satisfying all other criteria.

Other Eligibility Criteria for Inclusion

The following criteria must be met in addition to the revised free float requirement.

Eligible Securities - only equity shares listed on the Equity Shares (commercial companies) or Closed-ended investment fund categories, which have been admitted to trading on the London Stock Exchange with a Sterling, Euro or US Dollar denominated trading price on SETS, are eligible for inclusion in the FTSE UK Index Series. Shares listed in the Equity Shares (international commercial companies) secondary listing category are not eligible for inclusion.

Nationality Requirements - for UK incorporated companies, FTSE Russell will allocate UK nationality (a classification that determines a company's eligibility for inclusion in UK indices) provided the company has its sole listing in the UK and has a minimum free float of 10%.

For non-UK incorporated companies, FTSE Russell will allocate UK nationality provided that the company publicly acknowledges adherence to the principles of the UK Corporate Governance Code, pre-emption rights and the UK Takeover Code as far as practicable.

Price Screen - there must be an accurate and reliable price for the purposes of determining the market value of a company.

Minimum Voting Rights - companies assigned a developed market nationality are required to have greater than 5% of the company's voting rights (aggregated across all its equity securities, including, where identifiable, those that are not listed or trading) in the hands of unrestricted shareholders, or they will be deemed ineligible for index inclusion.

FTSE Russell will conduct an annual review of existing constituents in June each year based on data as of the last business day in April. Any constituent deemed to be failing the minimum voting rights’ requirement because of increased voting power (i.e. dual class share structures) will be removed from the FTSE UK Index Series in conjunction with the annual index review in June.

Investability Weightings / Free Float - constituents of the FTSE UK Index Series are adjusted for free float and foreign ownership limits (where applicable to UK investors).

Non-UK incorporated companies that were previously unable to meet the 25% free float threshold should assess whether they now satisfy the revised 10% minimum requirement and the other eligibility criteria outlined above ahead of the June 2026 index review. Companies considering a UK listing should also take these changes into account when evaluating the potential benefits of inclusion in the FTSE UK Index Series.

Equality (Race and Disability) Bill

Background

The consultation ran from 18 March to 10 June 2025 and sought views on the design of the reporting framework for large employers (those with 250 or more employees), including the metrics employers would be required to calculate and publish, how to define and compare relevant groups, alignment with existing gender pay gap reporting requirements, and whether action plans should be mandatory.

Support was substantial, with 87% of respondents in favour of mandatory reporting for large employers, and affirmed the government’s plans to proceed with mandatory reporting.

Ethnicity pay gap reporting

Employers will be required to publish pay comparisons across the five broad ethnic groups classified by the Office for National Statistics (ONS):

- White

- Asian or Asian British

- Black, Black British, Caribbean or African

- Mixed or multiple ethnic groups

- Other ethnic groups

Employers will also be required to publish a binary comparison between White (including White Other) employees and all other ethnic groups combined. A minimum threshold of employees will apply to each group being reported on to protect anonymity; policy work is ongoing to determine the most appropriate threshold.

Disability pay gap reporting

Employers will be required to publish a binary comparison of pay between disabled and non-disabled employees. Under the Equality Act 2010, a person is disabled if they have a physical or a mental condition that has a substantial and long-term impact on their ability to do normal day to day activities. For the reporting threshold, the government received differing views and will continue to work on what the most appropriate threshold should be.

Reporting metrics

The requirements will mirror those already in place for gender pay gap reporting. Employers will be required to disclose (i) mean and median differences in average hourly pay rates; (ii) mean and median differences in bonus pay; (iii) the percentage of employees receiving bonus pay; and (iv) the percentage of employees in each pay quartile.

The government plans to introduce detailed, step-by-step guidance for employers on how these calculations should be made, including any particular considerations which are relevant for ethnicity and disability data.

Related Capabilities

-

Corporate

-

M&A & Corporate Finance

-

UK Public Company